Revisions

June 3, 2026: Performance updates and changes to borrowing limits.

April 2, 2026: Polished for better readability.

April 1, 2026: Updated to reflect new minimum score.

March 5, 2026: Updated to reflect changes to late fees and recovery fees.

Temporarily short on cash and need a quick infusion for cash flow purposes? Or want to fund those in need while earning some money in the process? Learn the ins and outs of SoLo Funds, and how to use it effectively whether you’re a borrower or lender.

Introduction to SoLo Funds.

SoLo Funds is a peer-to-peer lending platform that connects borrowers with lenders. Users can register on the platform as a borrower or as a lender. Borrowers are able to submit loan requests, and lenders are able to choose who to fund. SoLo Funds is accessible through its mobile app or desktop website.

Links: Referral | Non-Referral

Signing up with the referral link gives you $5 towards your first loan and $5 when you repay as a borrower. As a lender, the referral link gives you $5 when you fund your first loan.

Using SoLo as a borrower.

When you sign up on the SoLo Funds platform, you’ll be prompted to perform identity verification and link your bank account. SoLo will use your personal information and bank account data to determine your creditworthiness. They do this through their own proprietary algorithms that analyze your financials for steady income, stable cash flow, and other related metrics. The system adheres to KYC and AML regulations as required by law.

The SoLo score ranges from 1 to 99. Your score needs to be at least 53 in order for lenders to see your loan request on the marketplace. You can boost your score by attaching additional payment methods and bank accounts to your profile. If your score isn’t at least 53 even after linking all of your accounts, SoLo doesn’t believe you have the ability to repay loans. You’ll be able to post a loan request, but lenders will not be able to see it. At that point, SoLo Funds is not a good fit for you, and you should look for an alternative instead.

If you meet all the requirements and have a score of 53 or higher, you can proceed. Before you start your first loan request, go into the settings page and toggle off the “SoLo Donation” option. Turning this setting off allows you to bypass the platform fee that they charge. When creating your loan request, set the lender tip to the maximum allowed amount (15% of the principal). The due date should be set as far out as possible, since paying your loan back early will boost your score higher. As a result, your borrowing limits will be lifted more quickly. As you build up positive repayment history on SoLo, you’ll eventually be able to borrow as much as $650.

Using SoLo as a lender.

The signup process as a lender is similar to signing up as a borrower. The only difference is that lenders do not receive a SoLo score. There is no need to determine your estimated ability to repay loans since you’re the one funding loans in the marketplace.

Lenders have the ability to filter the marketplace by SoLo score, tip percentage, loan amount, SoLo Lender Protection, and SoLo Boost. Personally, I only use the tip percentage filter, from 14% to 15% (cannot filter by 15% only) and sort the list by descending score (default sort). I only fund loans where the proposed lender tip is the maximum amount, which is 15% of the principal. Funding anything with a lower tip is not worthwhile since SoLo charges the lender (yes, the lender, not the borrower) a 12% late fee as soon as the borrower misses their due date.

Ideally, fund loans that have a score of 80 or higher. Even more importantly, take repayment history into account. Look through the user’s loan history and ensure they have been on the platform for a year or more. Stable repayment history is more important than a high score alone, as some users simply build up their score to request larger and larger amounts until they ultimately default.

If you choose to fund loan requests from users with low scores as part of your strategy, make the most of SLP (SoLo Lender Protection). When funding very high-risk loans, I opt into SLP for a 5% fee. In the case of non-repayment by the due date, SoLo pays out 90% of the principal and 90% of the SoLo Donation (if any) in the form of credit that you can put towards your next loan.

Keep in mind that SLP is a double-edged sword. A significant portion of the user base ends up paying loans late, which means you end up losing money with a partial payout if the user does end up repaying shortly after the due date. Conversely, receiving a partial payout is a good use of insurance if the user doesn’t end up repaying the loan, especially for borrowers who are brand new to the platform.

If a borrower becomes delinquent by more than 20 to 30 days (depending on the length of the loan), the lender is assessed a 35% recovery fee and the borrower is assessed a 15% late fee (payable to the lender). If the user eventually defaults on the loan (non-repayment after 90 days), the loan is forwarded to a debt collection agency. The debt collectors will apply a 35% fee to any money successfully recovered from the borrower.

Personal performance.

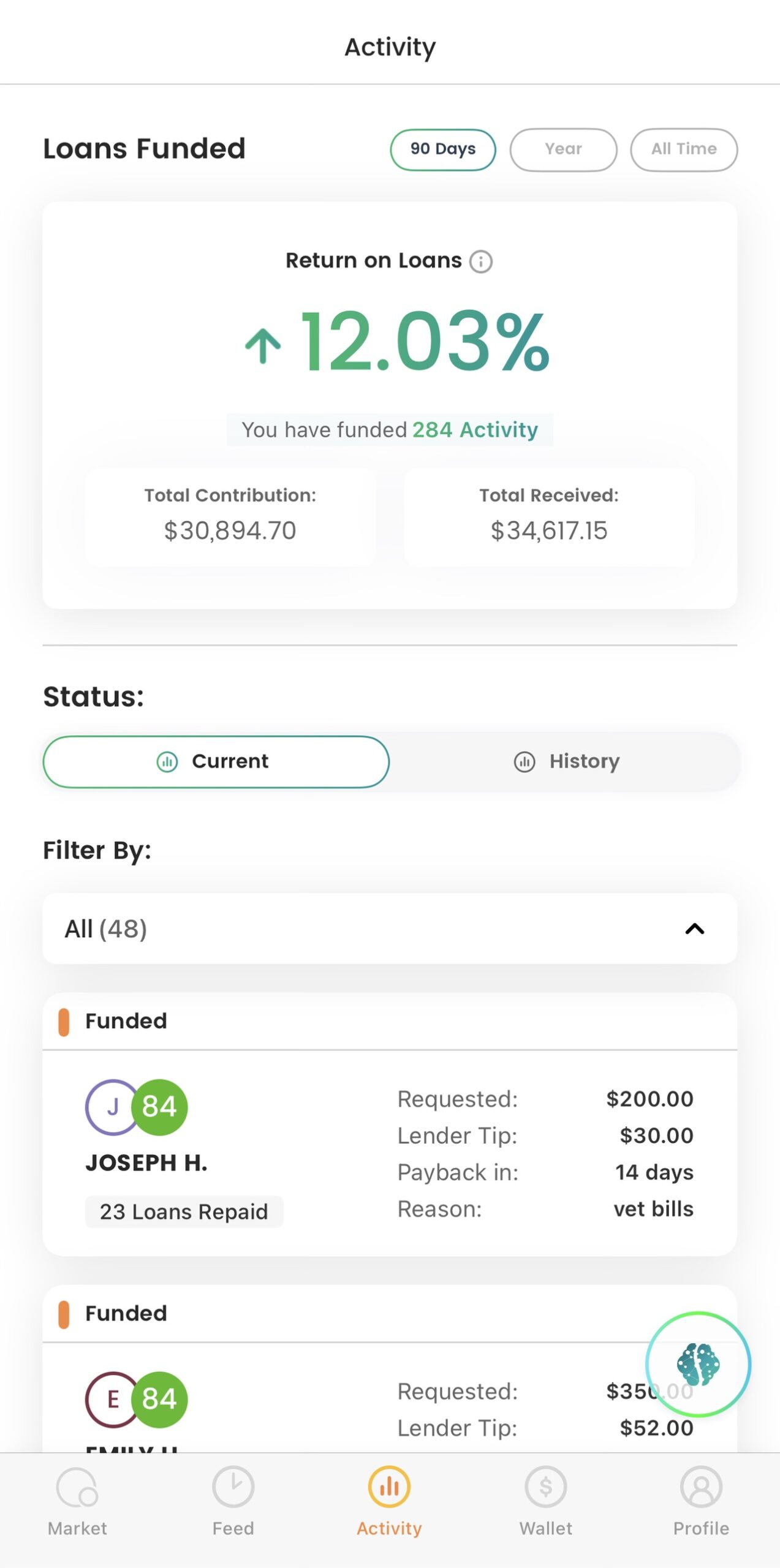

I’ve used SoLo Funds for three months now. I’ve funded 284 loans, so just slightly under a hundred loans per month on average. The SoLo dashboard shows that I’ve made $30,894.70 in total contributions, and I’ve received $34,617.15 in repayments so far. The total contribution value is inaccurate and should actually be a few thousand dollars higher since the amount displayed doesn’t include unsettled loans (currently active or overdue). Keep in mind that this performance is also inflated since the first 99 loans on the SoLo Funds platform are exempt from the 12% late fee, as a promotional offer to attract new lenders. I expect the performance to gradually drop and stabilize at a much lower rate of return. Here are the compiled stats so far.

Funded: 34 loans (not yet due)

Overdue: 14 loans (ranging from 2 days to 79 days past due)

Credited: 10 loans (SLP insurance, included in repayment total)

Late Repayment: 64 loans

On-Time Repayment: 162 loans

If we exclude the currently funded loans that are not yet due, we can calculate more accurate percentages for each category. About 6% (14/250) of loans are currently overdue, averaging about 36 days late. I’m expecting that the vast majority of these borrowers are not going to repay their loans, so that’s approximately $1,880 in losses (excluding SoLo Donations). About 4% (10/250) had SLP kick in. Six of the ten users actually ended up repaying after the insurance paid out, and the remaining four never repaid their loans. About 26% (64/250) of loans were repaid late (some have the 12% late fee applied, and some also have the 35% recovery fee applied). Lastly, about 65% (162/250) of borrowers repaid their loans on time (includes early repayments).

These are just my personal results based on my first three months of lending on SoLo. Your results may vary depending on your lending strategy, who you decide to fund, your risk tolerance, the amount of capital deployed, the number of users funded, and other factors. This side hustle is extremely high risk, but has the potential for a moderately high reward if executed well. In a single month, the return on investment could theoretically be up to 15%, which means one month could potentially outperform the average yearly return of the S&P 500. Of course, that’s an ideal scenario and is unlikely to happen in practice. Tread carefully and don’t risk more than you’re willing to lose.

June Update.

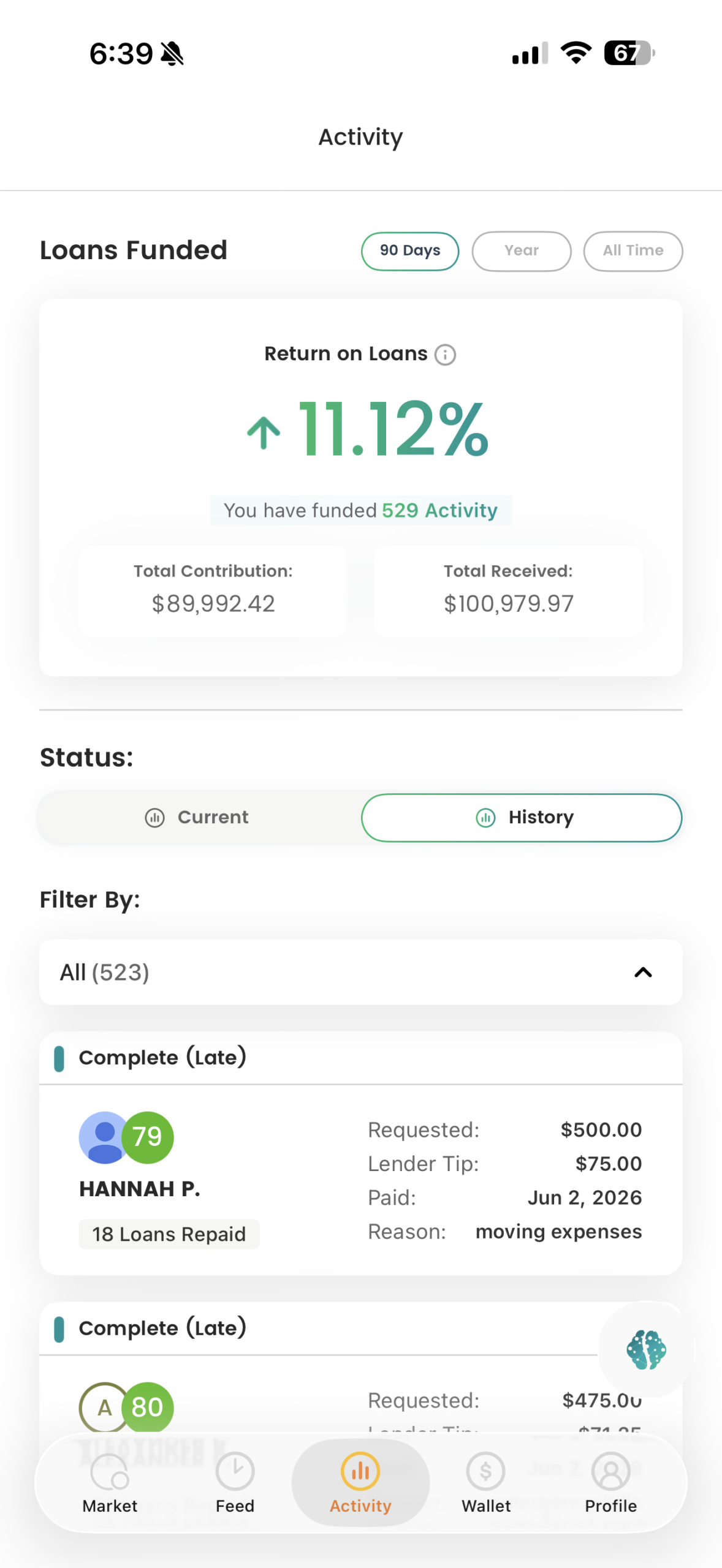

Four months have passed since I first wrote this blog post. My personal performance in the section above was from the beginning of February, and this update is for the beginning of June. I’ve broken the $100,000 milestone of “total received” so this is a nice stopping point for the final update. The “total contribution” figures don’t include loans that are currently active, and also don’t include loans that are currently overdue or defaulted. In the end, I’ve roughly broken even (with maybe just a tiny bit of profit), but the risk clearly does not outweigh the returns that you get from this platform.

In the SoLo Gold meetings, leadership has mentioned that they will be rolling out a “Impact Plus” product (most likely by the end of the 2026). They are targeting an average of 16% APY and the entire thing will be automated. There would be no need to manually choose which loans to fund, everything just works on autopilot. There will be a minimum of three-month blackout timeframes where you can’t withdraw your deposits or earnings. The biggest benefit of the upcoming offering is that returns will be guaranteed. It will be contractually obligated that you will incur zero losses. I’m looking forward to it, but these are all forward-looking statements and plans can drastically change. They claim that this service will start rolling out in one state and eventually be available in all states within a year of launch. Time will tell how that ends up.